S K Verma (*)

India – home to approximately 1.1 billion people with a fledgling middle class of approximately 350 million is often seen as one of the largest emerging markets on the globe. It is significant to note that a middle class population of 350 million is more than the entire population of the USA and close that of the European Union. This provides India with a distinct cutting edge. If we are to add population of those markets with which India has preferential trade or free trade arrangements, the market size is sure to cover more than one-fourth of the world population.

When looked at the Indian consumer market, not only that it has a significant size of middle class population, it also has 54% of population below the age of 25 years, i.e. a head count of over 500 million people, guaranteeing the future growth of availability of labour, productivity and consumerism.

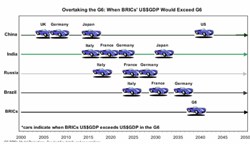

Goldman Sachs, renowned consulting group has put Brazil, Russia, India and China or in short BRIC as the group of countries which has started taking full charge of growth of the global economy. Considering the recent studies conducted on BRIC, India would overtake most of the G-8 countries in a few decades time from now starting with UK, Italy, France and Germany by the year 2025. One such study commissioned by Goldman Sachs came to the conclusion as depicted in the following graphical representation:

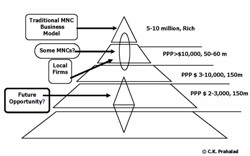

Most major trading nations in the world have always looked at India as a group of markets displaying different consumer preferences but governed by a single over arching trade regime. When calculated in terms of Purchasing Power Parity (PPP), India has the 4th largest economy in the world with a Gross Domestic Product (GDP) of over US$ 3.8 trillion (Source : World Bank), inching closer to take over Japan (US$3.9 trillion – Source : World Bank) for the third position. On the basis of PPP, the Indian consumers present a picture represented by the following graph:

The above depicts the market segments and opportunities available in the Indian market.

Currently, the Indian economy is growing at a rate which is second only to the Chinese in the world of emerging markets. Emboldened by a sustained economic growth over a long period, the Government of India has made premature re-payment of US$ 3 billion of high cost loan to the World Bank and the Asian Development Bank with the possibility of other similar loans being repaid prematurely. This squarely indicates the prevailing confidence in India. In recent past, vigorous growth over a strong market economic fundamental has characterized developments in the Indian economy in the financial year 2006-07 (financial year in India runs from 1st of April to 31st of March next year). Despite some concerns on inflation, a quick estimate puts the growth of GDP at 9.2%. The Asian Development Bank has predicted that India is likely to grow by more than 9% for the period 2007-12. This type of predictability is of essence to industry movers in the form of Foreign Direct Investment or as trading initiative. A recent snap-shot of the Indian economy could be found in the following table (Source: India’s Economic Survey 2006-07):

In the first three quarters of financial year 2006-07, export posted a growth of 36.3% with a volume of US$ 89.5 billion. The same figures for imports were 36.2% and US$ 131.2 billion respectively, out of which approximately US$ 44 billion was the cost of import of oil and natural gas. At the end of March 2007, India’s foreign exchange reserve touched US$198 billion.

According to a report recently released by Forbes, India has 36 billionaires with the combined assets of US$ 192 billion, the highest figures in Asia.

It is not easy to profile Indian economy in limited words and, therefore, the author’s intention is to give the readers only an overview of the same in the following paragraphs. Following are key developments in some selected sectors of the Indian economy:

AGRICULTURE

India is largely an agricultural society with a large population depending on agricultural and allied industry for its livelihood and sustenance. With the second largest arable land area in the world, India is the largest producer of milk, pulses, sugarcane and tea. It produces more than 33 million tons of fruits and 62 million tons of vegetables. The total size of food market in India is estimated to be US$92 billion with that for processed food to be US$30 billion.

India is the leading livestock country in the world. It ranks first in the cattle (including buffaloes) population, second in goats and fourth in the sheep population.

Looking at the competence of major players in food processing industry in Turkey, India offers an excellent opportunity for setting up food processing units.

INDUSTRY

The index of Industrial production for the period April – November 2006 reveals a strong sustained growth of the Indian industry. The general index on industrial production shows a rise of 10.6% in the first 8 months of the financial year 2006-07 against 8.3% growth seen in the corresponding period of the last financial year. The industrial sectors that have displayed growth much higher compared to the growth in the corresponding period of previous financial year are basic metals (20.4%), transport equipment (16.3%), machinery equipment (14.1%), non-metallic products (13.7%), cotton textiles (13.1%), rubber and plastic products (11.9%), metal products (6.8%) and wool (6.6%).

AUTOMOBILES

India is not only a huge market for the passenger car sector; it is also one of the major players in the global auto components business. The auto industry was worth 34 billion US dollar in 2006 growing at a CAGR of 14% over the past five years. The total number of vehicles sold exceeds 9 million and is expected to grow further. According to the industry experts, if the current trends continued, the Indian auto manufacturers should be able to sell more than 10 million vehicles in the present calendar year. India is the 2nd largest two-wheelers market in the world. India is the 4th largest commercial vehicle market in the world. The current market size of passenger cars put India at the 11th spot which is expected to move upward to the 7th rank by 2016.

The installed capacity of the automotive industry has been growing at a compounded annual rate of over 16 per cent since 2001-02. It produced a wide variety of vehicles including 1.7 million four wheelers (passenger cars, light, medium and heavy commercial vehicles, multi-utility vehicles such as jeeps) and over 8 million two and three wheelers (scooters, motor-cycles, mopeds, and three wheelers) in 2005-06.

The India automobile sector has witnessed investments coming in from various world leaders both for manufacturing and research and development. Mercedes, BMW, Porsche, Audi, Bentley and Rolls Royce are already selling in India. In addition, German luxury car maker Audi AG is preparing to enter as well. This is not including those companies which have manufacturing facility in India such as Nissan, Toyota, Honda, Hyundai, GM, etc. The Indian automobile major TATA is already in the Turkish market with Mahindra & Mahindra trying to do the same. Mahindra & Mahindra has emerged as the 4th largest tractor brand in the US in the 15-90 horse power segments. India’s competitive advantage does not come from cost alone. It is about Full Service Supply (FSS) capability. As products life cycles and lead time for product developments shrink, Indian manufacturers have evolved from build to print to customize offerings.

AUTO-COMPONENTS

The Indian auto component industry is likely to almost double to US$ 18.7 billion by 2009 and reach about US$ 40 billion by 2014. Its globally competitive auto component manufacturing sector has been much in demand with global auto majors. A number of them source critical components from India, with engine parts making up nearly a third of all exports:

• Engine parts (31 per cent)

• Drive transmission and steering parts (19 per cent)

• Body and chassis (12 per cent)

• Suspension and braking parts (12 per cent)

• Equipment (10 per cent)

• Electrical parts (9 per cent)

• Others (7 per cent)

In 2006, components worth US$2 billion were exported by Indian companies, 75 per cent of which were bought directly by car companies. The original equipment manufacturers (OEMs) include firms like General Motors, Ford Motor Company, Cummins International, Bosch, Volkswagen, BMW, MAN (trucks) and JCB (earthmoving equipment) amongst others.

ENERGY

The petroleum and natural gas sector is estimated worth US$ 90 billion in India. India’s crude refining capacity will increase from 127 MTPA to 141.70 MTPA by the end of 2007. India imports about 75% of its requirement of crude petroleum. However, with the help of 25 refineries having 2.5 million barrel per day of refining capacity, it continues to have a net exportable surplus in refined petroleum products. By 2010, India is projected to emerge as the 4th largest consumer of energy, after the US, China and Japan. The Indian oil companies have various regional and global tie-ups which assist to satisfy the ever growing demand of energy in India. Indian Oil Corporation Limited has planned to invest US$6 billion in a refinery in Ceyhan producing 15 MTPA of refined petroleum products. Over and above, Indian Oil Corporation Limited is close to concluding an agreement with the promoters of Trans Anatolian Pipeline Company (TAPCO) of Turkey to take 12.5% stake in the US$1.5 billion pipeline from Samsun to Ceyhan.

GEMS AND JEWELLERY

India is the largest diamond cutting and polishing center in the world, with predicted growth of between 15% and 20% for many years to come. Overall export from this sector was approximately US$ 16 billion last year. According to a study by the consulting firm McKinsey, the branded jewellery market in India would reach US$2.28 billion by 2010, over and above, market for the non-branded jewellery is worth approximately US$10 billion. Accounting for 20% of world consumption of gold, India is the largest consumer of the yellow metal.

Destination wise, the major market for Indian gems and jewellery in terms of importance are USA, UAE, Hong Kong, Belgium, Israel, Japan, Thailand, UK, Singapore and Korea. The US accounts for 29 per cent of the total exports from India in this sector.

INFORMATION TECHNOLOGY

India’s prowess in the Information Technology sector has been proved time and again in the world market. It is expected that this sector would reach a figure of US$ 54 billion by the year 2008, with a Cumulative Annual Growth Rate (CAGR) of 21.1%. The total number of professionals employed in the Information Technology and Enabled Service sectors is estimated to exceed 1.2 million. Few interesting facts in this sector are as follows:

(a) Google, the word’s largest search engine has set up a Research and Development Center in Bangalore.

(b) The US based chip maker Intersil is in the process of setting up of a Design Center in India.

(c) Mobile phone giant Nokia has set up three R&D labs in India.

(d) Leading Web portal Yahoo carries out R&D work in Bangalore.

(e) IBM has one of the 8 worldwide innovation labs in India.

Closely following the growth in the software sector, the Indian PC market grew by over 24% last year.

India has proven its significant presence in the cyber-industry over and over again. Business Process Outsourcing (BPO) has been one of the main-stays of the industry. This includes both back office operations and research and development outsourcing. The later has been growing with a remarkable pace recently. It includes all segments of various industries.

MEDIA & ENTERTAINMENT

The current size of the industry as a whole is estimated US$ 8 billion and is expected to grow at a CAGR of 14%. The film, entertainment and television segment dominate the industry followed by the print, radio and music segments. The Indian film industry is the largest in the world with over 1000 films produced in the year 2006. The animation business in India is also growing at a rate exceeding 20% per annum. Indian print media industry brings out about 900 news publications for a combined readership of 200 million. Television has dominated the entertainment and media industry and continues to have the potential to do so even in the future. With over 200 million households, TV connection is there for about half of them. With an average household size of 4-5, the potential for advertiser is immense. About 61 million households are connected through cables and satellites giving rise to a fledgling domestic cable and satellite industry. More than 300 channels are beamed into Indian sky for cable satellite users to view. A PriceWaterCooper study suggests that there will be a boom in a radio industry with 22% growth resulting in trebling the current size to US$ 146 million by 2009.

PHARMACEUTICAL AND HEALTHCARE

The size of the Indian pharmaceutical industry is approximately US$9 billion (on the basis of revenue). India is emerging as a strong and key global player in both generic medicine and formulation alike. The Indian pharmaceutical industry has the higher number of manufacturing plants approved by Food and Drug Administration (FDA), anywhere outside the USA. It has the largest number of Drug Master File (DMF) as well.

The healthcare market is also undergoing a strong and qualitative transformation. The healthcare market is expected to grow from US$22.2 billion at present to US$50 billion by 2012. The competence of Indian doctors and healthcare practitioners could be judged from the fact that a very large number of doctors and healthcare practitioners in both the USA and the UK are from India.

REAL ESTATE

The Real Estate and Construction is US$14 billion industry in India. The global real estate consultants Knight Frank has ranked India 5th in the list of 30 emerging markets and has predicted an impressive growth of 20% for the organized retail estate sectors in India. Merrill Lynch has said in a study that the number of malls in Mumbai, Bangalore, New Delhi, Hyderabad and Pune will grow to 250 by the year 2010 as against 50 now.

RESEARCH AND DEVELOPMENT

India is poised for more than 125 Fortune 500 companies for conducting their research and development there. These include research and development into frontier areas of satellite fabrication, mobile telephony, nano-technology, bio-technology, IT hardware, pharmaceuticals, etc. As an indication of India’s strength in the frontier areas of research and development, 65 institutions in India are engaged in carrying out only the genetic engineering research. India is one of the 6 countries in the world to manufacture and launch its own satellite. India has launched satellites for other countries including Germany and Korea as well. Swedish bus and truck maker Volvo has opened the technology center and a product development unit in Bangalore. A number of semi-conductor companies, both fab and fabless have either set up or outsourced their research and development in India. Such work includes ab-initio design, CAD, simulation, testing and fabrication. New sectors growing at a fast rate include cutting edge technologies such as embedded software, nano-technology, avionics, etc.

STEEL

India is among the 10 top global suppliers of aluminium and steel in the world. About 35 million ton of steel is produced in India. It is the largest producer of sponge iron in the world. In some of the recent developments, India’s private sector steel giant TATA Steel has been given approval to start construction of its US$ 103 million ferrochrome steel plant at Richards Bay in South Africa. TATA has also acquired NATSTEL of Singapore, Corus Steel and has planned for further acquisitions in Vietnam and Thailand. All these have made it the 5th largest steel company in the world. Mittal Steel which recently acquired Arcelor is the fastest growing steel manufacturing company in the world. They have many more acquisitions planned in coming years. Another steel maker ESSAR is also making new inroads by expanding its production capacity both in India and abroad.

TELECOMMUNICATIONS

The number of telephone users registered is approximately 190 million, counted up to December 2006. Growth of the total phone subscription sustained largely on the growing mobile phone communication. India is adding approximately 6 million mobile connections every month and the total mobile connections stand at approximately 150 million. It is expected to increase to 250 million by the year 2009-10. Almost all the international names are present in the Indian telecom market but Indian domestic companies still retain the lead. The call-charges for mobile connectivity are as low as 0.025 YTL (or USD 0.020) per minute.

TEXTILES

Textile sector is a US$ 36 billion industry in India. It boasts about 25% share of world trade in cotton yarn and fabrics. It is expected that it would reach potential size US$ 85 billion by 2010, with a domestic market size of US$ 45 billion.

Production of fabrics increased by 9.25 per cent in the financial year 2005-06 and, up to November 2006, by 8.20 per cent over the corresponding period of the previous year.

In US dollar terms, the value of exports increased by 21.8 per cent in 2005-06 and 11.7 per cent up to September 2006.

Already, the Government's Textile Policy looks at textile and apparel exports of US$ 50 billion by 2010-of which garments will bring in US$25 billion. The main markets for Indian textiles and apparels are the US, UAE, UK, Germany, France, Italy, Russia, Canada, Bangladesh and Japan. A series of progressive measures have been planned to strengthen the textile sector in India: • Technology Mission on Cotton (TMC) • Technology Up-gradation fund Scheme (TUFS) • Reduction in customs duty on import of state-of-the-art machinery • Debt Restructuring Scheme • Setting up of Apparel Training and Design Centres (ATDCs) • 100 per cent Foreign Direct Investment (FDI) in the textile sector under automatic route.

MULTINATIONALS IN INDIA

Some of the major Fortune 500 companies in India are ABB, Allianz, ABN Amro, Alstom, British Petroleum, BASF, Bombardier, CISCO, Coca-Cola, Citigroup, Dupont, Electrolux, Ford, Federal Express, GE, GSK, General Motors, HSBC, Honeywell, IBM, Intel, Johnson & Johnson, Lafarge, LG, Metlife, MICO, Microsoft, Nestle, Novartis, Pepsico, Philips, Pfizer, Prudential, Saint Gobain, Samsung, Sony, Shell, Siemens, Toyota, Unilever, Visteon, Volvo, Whirlpool etc.

Some of the major German companies in India are Abicor Binzel, Adidas Marketing, Baerlocher Additives, Bajaj Allianz, Basf Baumuller, Bayer, Beiersdorf, Bosch Group, Braun Medical, Burgmann, Carl Bechem, Carl Zeiss, Daimler Chrysler, DHL Express, DMG, Durr, Fichtner, Henkel, Kluber Lubrication, Knorr Bremse, Lahmeyer International, Lapp, Pharmaplan Schuler Steag Encotec Stollberg, Suspa Pneumatics, Wurth Zeppelin Mobile Systems, Zwick Roell etc.

Some of the major British companies in India are Aviva, Barclays, BP, British Telecom, Cable & Wireless, Cadbury India, Cairn Energy, GSK Pharmaceuticals, HSBC, ICI India, Johnson Matthey, Logica CMG, Marconi Telecom, Marks & Spencer, P&O Ports, Reuters, Scope International, Shell India, Standard Chartered Bank, Tesco, Unilever, Virgin Atlantic etc.

INDIAN MULTINATIONALS

Altogether Indian companies have acquired assets worth US$24 billion in the first nine months of FY 2006-07. The figure for the whole of 2005 was US$18 billion.

Continental Engine, Sundram Fasteners (SFL), Tata Motors, Ranbaxy, Dr Reddy’s Laboratories, Asian Paints, Bharat Forge, Essel Propack, Tata Consultancy Services (TCS), Infosys, Wockhardt, Cadila Health, Apollo Healthcare, Sun Pharma, Hindalco, Wipro, Aditya Birla, United Phosphorus, Indian Oil Corporation Limited, ONGC, Tata Steel, Mittal Steel, ESSAR, APTECH etc. are some of the Indian companies who have major interests and assets in countries other than India. They are truly Indian multinationals.

It is very important to understand that unlike many other economies, India’s economic growth is mainly driven by the domestic market. However, since the past decade, foreign trade too has started playing an increasingly significant role in the improved economic scenairo.

* Counselor, Embassy of India, Ankara